Key Takeaways

- Default treatment is a receivable: Most EOSB advances should be recognised as financial assets under IFRS 9, not netted against the DBO.

- Three possible treatments: Depending on the facts, an EOSB advance is either a receivable (most common), a secured loan, or a settlement.

- Settlement requires extinguishment: Under IAS 19, netting an advance against the DBO is only valid if the employee’s underlying entitlement is permanently reduced.

- Documentation is critical: Without a written agreement, recovery rights under Article 92 of Saudi Labour Law may not apply, significantly increasing credit risk.

- Present gross when in doubt: If documentation is unclear or recovery rights exist, present the DBO gross and the advance as a separate receivable.

Table of Contents

- Introduction

- The Three Possible Treatments

- The Decision Framework

- Summary

- Red Flags for Auditors

- Disclosure Requirements

- FAQs

1. Introduction

End of Service Benefit (EOSB) schemes are a defining feature of employment across the GCC. In Saudi Arabia, EOSB is governed by Article 84 of the Labour Law: half a month’s wage for each of the first five years of service, and one month’s wage for each subsequent year, calculated on the employee’s final basic salary.

In practice, employers sometimes pay advances to employees against their future EOSB entitlement—to support a housing deposit, family emergency, or other significant expense. The expectation is that the advance will be recovered from the employee’s final EOSB when they leave.

The EOSB advance payment accounting question that follows is not as straightforward as it appears. The instinctive treatment—netting the advance against the Defined Benefit Obligation (DBO)—is rarely correct under IAS 19.

This article sets out a structured framework to determine the appropriate treatment. The principles apply equally to EOSB schemes in the UAE, Qatar, Oman, Bahrain, and Kuwait, though the specific labour law references here are KSA-focused.

2. The Three Possible Treatments

Regulatory Context

In Saudi Arabia, EOSB is governed by the Labour Law:

| Article | Provision |

|---|---|

| Article 84 | EOSB entitlement: ½ month per year for first 5 years, 1 month per year thereafter |

| Article 85 | Resignation entitlements: ⅓ (2–5 years), ⅔ (5–10 years), full (10+ years) |

| Article 92 | Permits deductions from EOSB for loans/advances, with a written agreement |

Under IAS 19, the Defined Benefit Obligation (DBO) is the present value of future payments required to settle the obligation arising from past service. This is critical: the DBO represents what the employer expects to pay when the employee eventually exits. An advance paid today is a past cashflow—it does not reduce the future payment the employee is entitled to receive, and therefore has no direct impact on the DBO.

The Three Treatments

Given this, there are three ways an EOSB advance can be accounted for:

Receivable (IFRS 9): The advance is a financial asset—a loan to the employee that happens to be secured against their future EOSB. The DBO remains unchanged; the advance sits separately on the balance sheet. This is the default treatment and applies in most cases.

Secured Loan (IFRS 9): A variant of the receivable treatment, but with a formal written agreement and clear recovery rights. The accounting is the same—gross DBO plus separate receivable—but the documentation reduces credit risk and supports lower ECL provisioning.

Settlement (IAS 19): The advance genuinely reduces the employee’s benefit entitlement when he/she leaves. The DBO is recalculated, a settlement gain or loss is recognised, and there is no receivable. This treatment is rare and requires specific conditions to be met.

The Key Distinction

The legal right to deduct an advance from final EOSB (under Article 92 of Saudi Labour Law) does not mean the advance can be treated as a settlement under IAS 19. The two questions are separate:

- Legal: Can the employer recover the advance? (Yes, with a written agreement)

- Accounting: Has the obligation been extinguished? (Only if the underlying entitlement is reduced)

Most advances satisfy the first but not the second.

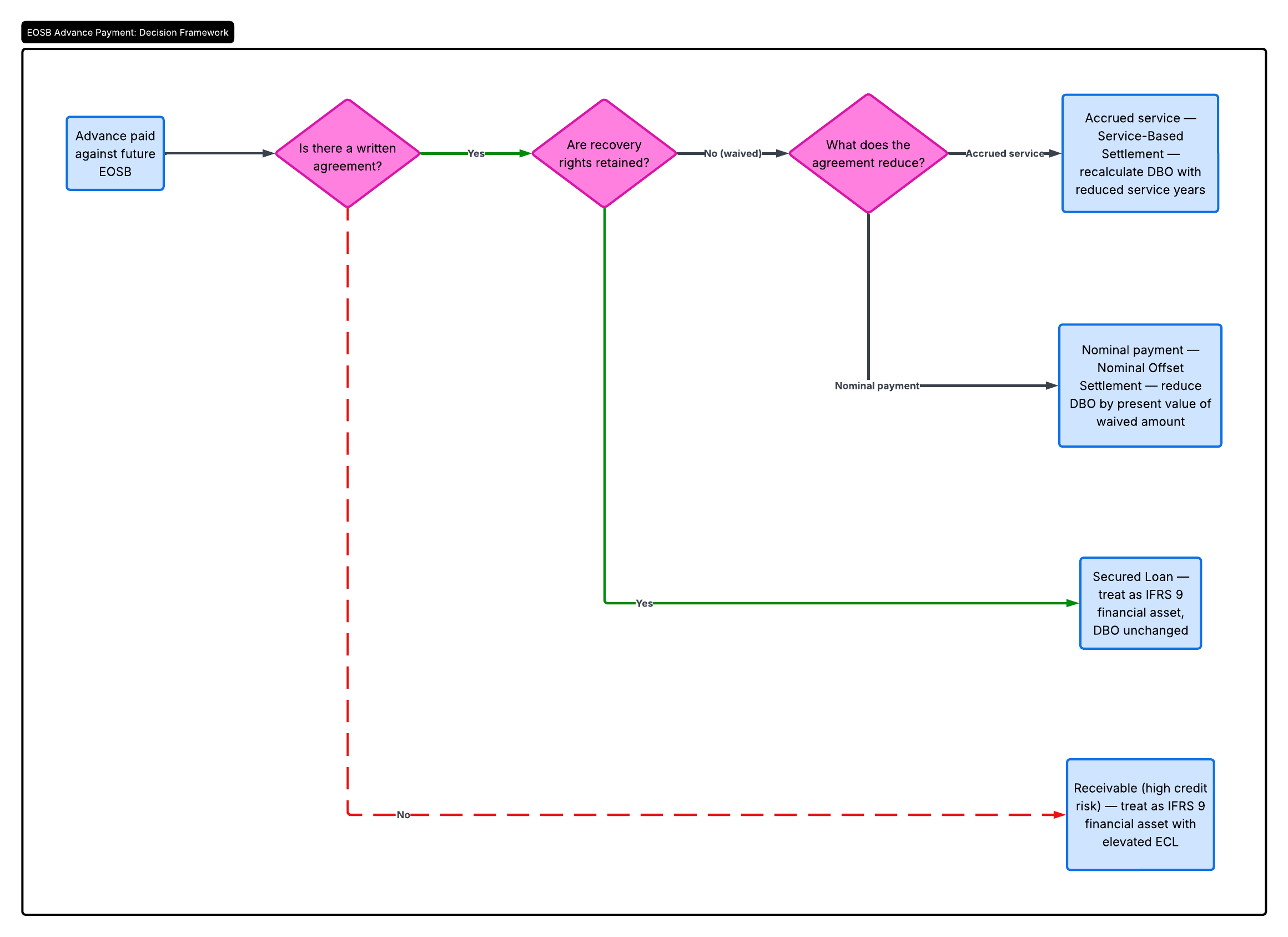

3. The Decision Framework

We have seen companies rushing to adopt a settlement approach for accounting of these advance payments. The correct EOSB advance payment accounting treatment depends on three sequential questions:

- Is there a written agreement? Without documentation, there is no basis for settlement accounting—and even basic recovery rights under Article 92 may be unenforceable.

- Are recovery rights retained? Recovery rights are the employer’s contractual ability to reclaim the advance from the employee in various exit scenarios—resignation, termination for cause, death in service, etc. If the employer can pursue recovery in any scenario (even just termination for cause), the advance is economically a loan, not a settlement.

- If recovery rights are waived, what is reduced? A genuine settlement requires reducing the employee’s underlying entitlement—either their accrued service years or the nominal amount payable at exit. Simply agreeing not to recover the advance is not enough; the employee must give something up.

The combination of answers determines the treatment. The sections below walk through each scenario.

3.1 No Written Agreement

Scenario: An advance has been paid but there is no formal written agreement governing recovery.

Treatment: Receivable under IFRS 9 (high credit risk)

A settlement under IAS 19 requires the employer’s obligation to be extinguished. Without a written agreement, there is no documented basis for any reduction in the employee’s entitlement—the employee’s full statutory EOSB entitlement remains intact under Article 84.

What the employer has, in substance, is an informal receivable from the employee.

Accounting Treatment

| Element | Treatment |

|---|---|

| Defined Benefit Obligation | Unchanged; presented gross |

| Advance | Recognised as a financial asset under IFRS 9 |

| Initial measurement | Fair value at inception |

| Impairment | Higher ECL provision warranted given lack of documentation |

| Presentation | Separate asset; not netted against DBO |

Audit Alert

The absence of a written agreement is a control weakness. Without documentation:

- Recovery is harder to enforce if disputed

- Article 92 deduction rights may not apply

- Risk of full write-off is materially higher

- Inconsistent treatment across employees is likely

3.2 Agreement with Recovery Rights Retained

Scenario: A written agreement exists, and the employer retains recovery rights in at least some exit scenarios.

Treatment: Secured loan under IFRS 9

This is the most common arrangement in practice and the cleanest from an EOSB advance payment accounting perspective. The advance is economically a loan to the employee, secured against their future EOSB entitlement. The DBO continues to represent the full obligation; the receivable represents the employer’s right to be repaid.

Accounting Treatment

| Element | Treatment |

|---|---|

| Defined Benefit Obligation | Unchanged; presented gross |

| Advance | Financial asset under IFRS 9 |

| Initial measurement | Fair value (PV of expected recovery at market rate) |

| Subsequent measurement | Amortised cost; unwind discount as interest income |

| Below-market interest | Difference at inception treated as employee benefit cost |

| Impairment | ECL based on probability of non-recovery scenarios |

Behaviour at Exit

| Exit Type | Recovery Position | Accounting Impact |

|---|---|---|

| Resignation after 2 years (Article 85) | Deducted from EOSB; balance paid | Receivable extinguished against EOSB liability |

| Resignation before 2 years | Recoverable in full from employee | Receivable retained; impair if uncollectible |

| Termination for cause (Article 80) | Recoverable in full from employee | Receivable retained; impair if uncollectible |

| Death in service | Per agreement terms | Per terms of agreement |

| Force majeure (Article 87) | Full EOSB payable; advance deducted | Receivable extinguished against EOSB liability |

Key Auditor Questions

- Does the written agreement clearly set out recovery rights in each exit scenario?

- Is there evidence of consistent treatment across the employee population?

- Has the receivable been measured at fair value at inception (not just face value)?

- Does the ECL calculation reflect the probability of exit scenarios where recovery is uncertain?

- What happens if the advance exceeds the accrued EOSB at the date of exit?

3.3 Waiver Reducing Accrued Service

Scenario: A written agreement waives recovery rights and reduces the employee’s accrued service period in exchange for the payment.

Treatment: Service-based settlement under IAS 19

The employee’s underlying entitlement is reduced—they have formally given up a defined portion of their accrued service. Since the DBO is calculated with reference to service years, reducing service genuinely extinguishes part of the obligation.

Accounting Treatment

| Element | Treatment |

|---|---|

| Defined Benefit Obligation | Recalculated using reduced service period |

| Cash paid | Removed from balance sheet |

| Settlement gain/loss | Difference between cash paid and reduction in DBO, recognised in P&L per IAS 19.109–111 |

| No receivable | Cash is gone; no recovery right |

Worked Example

An employee has 10 years of accrued service. The DBO based on 10 years is SAR 500,000. The employer pays SAR 100,000 in exchange for a formal waiver of 2 years of accrued service. The DBO is recalculated based on 8 years: SAR 400,000.

| Item | Amount (SAR) |

|---|---|

| Cash paid | 100,000 |

| Reduction in DBO | 100,000 (500,000 − 400,000) |

| Settlement gain/loss | Nil |

If the recalculated DBO had been SAR 410,000, the settlement would produce a loss of SAR 10,000 (paid 100,000 to extinguish only 90,000 of obligation).

Documentation Required

- Written agreement signed by both parties

- Explicit waiver of any recovery rights, in any circumstance

- Formal amendment to the employee’s service record

- Board or senior management approval

Why Service-Based Settlements Are Rare

- Employers usually want to retain recovery rights

- Article 84 entitlements may not be straightforwardly reducible by private agreement (legal advice should be obtained)

- Administrative burden is significant

3.4 Waiver Reducing Nominal Payment Only

Scenario: A written agreement waives recovery rights and reduces the final nominal payment by the advance amount, without reducing accrued service.

Treatment: Nominal offset settlement under IAS 19

The employee’s accrued service is unchanged. What changes is the future nominal payment: the final EOSB cheque will be reduced by the advance amount when the employee exits.

The DBO Reduction Is Not the Cash Amount

This is where intuition fails. The DBO is the present value of the future obligation. If the future payment reduces by 100 (nominal), the DBO reduces by the present value of 100 over the period to expected exit.

Worked Example

| Item | Value |

|---|---|

| Cash paid today | SAR 100,000 |

| Expected period to exit | 5 years |

| Discount rate | 5% |

| Reduction in future nominal payment | SAR 100,000 |

| Reduction in DBO | SAR 100,000 / (1.05)⁵ ≈ SAR 78,350 |

| Settlement loss | SAR 100,000 − 78,350 = SAR 21,650 |

The settlement loss reflects the time value of money—the employer has paid 100,000 today to extinguish an obligation worth only 78,350 in present value terms.

Substance Over Form

A nominal offset settlement is economically similar to a non-recoverable interest-free advance. Auditors should scrutinise these arrangements:

- Is the “waiver” genuine, or is it a form of words on what is really a non-recoverable advance?

- Why has the employer chosen to recognise an immediate settlement loss rather than treat it as a loan?

- What is the commercial rationale for paying 100,000 today to extinguish a smaller present value obligation?

In many cases, recharacterisation as a non-recoverable advance (employee benefit expense) may be more appropriate than settlement accounting.

4. Summary

Decision Framework at a Glance

Decision framework for EOSB advance payment accounting

Decision framework for EOSB advance payment accountingScenario to Treatment

| Scenario | Written Agreement? | Recovery Rights? | What Is Reduced? | Treatment | DBO Impact |

|---|---|---|---|---|---|

| Informal advance | No | N/A | Nothing | Receivable (high ECL) | None |

| Documented advance | Yes | Retained | Nothing | Secured loan | None |

| Service waiver | Yes | Waived | Accrued service | Settlement | Recalculate with reduced service |

| Payment waiver | Yes | Waived | Nominal payment | Settlement | Reduce by PV of waived amount |

The default is gross presentation. Only where recovery rights are waived and the entitlement itself is reduced does the DBO change.

5. Red Flags for Auditors

| Red Flag | Treatment Likely Misapplied | Correct Response |

|---|---|---|

| No written agreement, but DBO netted | Settlement (no documentary basis) | Recharacterise as receivable; raise control weakness |

| Recovery rights retained, but DBO netted | Settlement (obligation not extinguished) | Recharacterise as secured loan |

| Advance exceeds accrued EOSB | Receivable underprovided | Higher ECL on the unsecured excess |

| Net presentation without disclosure | Likely IAS 32 offsetting breach | Gross presentation; separate disclosure |

| Advance shown as a plan asset | Plan asset definition misapplied | Reclassify to receivable |

| Inconsistent treatment across employees | No formal policy | Recommend formal policy and consistent application |

| “Settlement” without service or payment reduction | No basis for DBO reduction | Recharacterise as receivable |

6. Disclosure Requirements

Where advances are material, IAS 19 disclosure requirements (paragraphs 135–147) and IFRS 7 disclosures on financial assets apply. The financial statements should make clear:

- The existence of the advance arrangement

- The accounting treatment adopted

- Any judgements made (particularly around recoverability or settlement classification)

- The carrying amount of any related receivable

Sample Disclosure (Secured Loan Treatment)

The Company has paid advances to certain employees against their future End of Service Benefit entitlements. These advances are recoverable from the employee’s final EOSB on exit, in accordance with written agreements and Article 92 of the Labour Law. The advances are recognised as financial assets measured at amortised cost under IFRS 9, with an expected credit loss provision reflecting the probability of non-recovery scenarios. The Defined Benefit Obligation is presented gross of these advances; the related receivable is included within other receivables.

7. FAQs

Can EOSB advances be shown as plan assets?

No. Plan assets under IAS 19 are narrowly defined as assets held by a legally separate fund or qualifying insurance policies. Advances paid directly to employees do not qualify. They should be recognised as financial assets (receivables) under IFRS 9.

Is it ever acceptable to net the advance against the DBO?

Only if the employee’s underlying entitlement has been genuinely reduced—either through a reduction in accrued service or an irrevocable waiver of future payment amount. If the employer retains any recovery rights, the DBO should be presented gross with the advance as a separate asset. Note that even if the advances are treated as settlements, you wouldn’t just subtract the nominal amount of advances from the DBO. Instead, you would need to calculate the actuarial value of the amount of future benefit entitlement that has been extinguished.

What if the advance is immaterial?

Materiality applies as usual. However, even immaterial advances should follow the correct accounting treatment. An incorrect treatment that is immaterial today may become material as the practice scales, and consistency in policy is important for audit purposes.

How should ECL be calculated for EOSB advances?

When EOSB advance payments are deemed to be receivables or loans, they are outside the scope of IAS 19 and would fall under IFRS 9. ECL should reflect the probability of scenarios where full recovery is uncertain. Key inputs include:

- Historical data on early departures, resignations before vesting, and terminations for cause

- Whether the advance exceeds the employee’s current accrued EOSB

- Quality of documentation and enforceability of recovery rights

Does this framework apply outside Saudi Arabia?

Yes. The IAS 19 and IFRS 9 principles are universal. The labour law references differ—UAE uses Article 51 of Federal Decree-Law No. 33 of 2021, Qatar uses Article 54 of Law No. 14 of 2004, etc.—but the accounting decision framework is the same: does a written agreement exist, are recovery rights retained, and what exactly is reduced?

Should advances be included in benefit payments?

Yes, but only where the advance qualifies as a settlement. In those cases, the advance should be reported as a benefit paid for settlement, not as a regular benefit payment. The cash amount paid is the settlement payment; the reduction in DBO is the present value of the obligation extinguished. The difference between the two is recognised as a settlement gain or loss in P&L. For advances treated as receivables or secured loans, there is no benefit payment—the cash is a loan, not a settlement of the obligation.

Need Help With EOSB Advance Payment Accounting?

If you’re dealing with complex EOSB advance arrangements and need support with the accounting treatment or actuarial valuation, get in touch with our team. We work with finance teams across Saudi Arabia and the GCC on IAS 19 compliance and employee benefit valuations.