For many companies, this is the time to finalise their interim accounts for the first quarter of the current financial year. It is important to understand the movement in discount rate during this period to make an appropriate provision towards employee benefits liabilities.

Source of the discount rate for actuarial valuation

Companies often have to set the discount rate by choosing one source from a myriad of alternative sources, which often conflict with each other. Most of these sources are not relevant for the purposes of actuarial valuation, because they don’t depict the full term-structure of yields (or interest rates) or are not calibrated for the Indian economy.

Numerica uses the yield curves published by the Clearance Corporation Of India (CCIL) derived from the trades in GoI bonds on the National Stock Exchange (NSE). The yield curves produced by NSE/CCIL have been in use for over two decades now and are considered to be the true reflection of the interest rates in the Indian economy.

Numerica regularly collates and publishes the prevailing discount rates on this webpage.

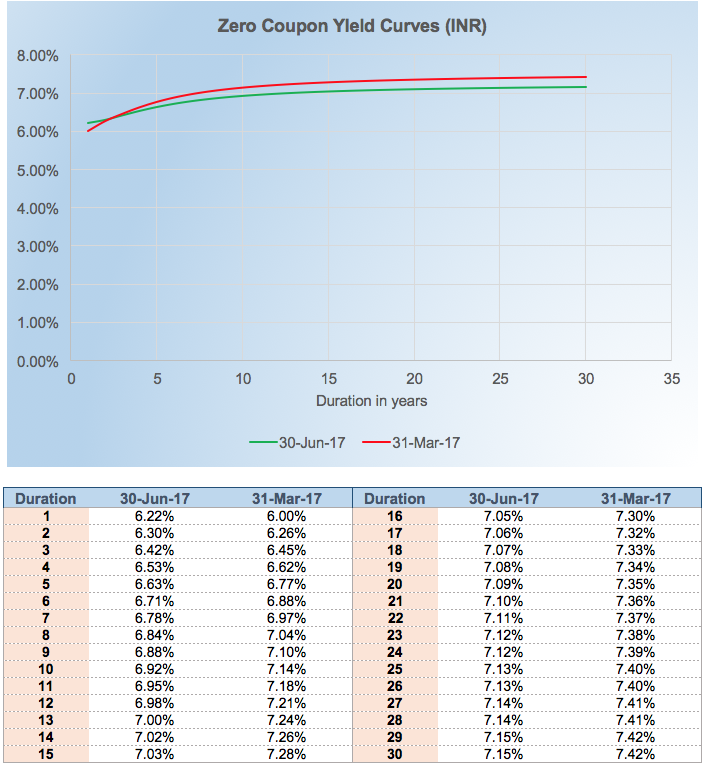

Comparison of yield curves: 30 Jun 2017 vs 31 Mar 2017

The discount rate as at any particular valuation date is read from the yield curve of GoI bonds as at that date.

The yield curves as at 31 March 2017 and 30 June 2017 are shown in the chart below. For smaller durations (less than three years), the yields have increased slightly during the first quarter. Beyond three years, the yields have generally reduced.

(Source: Clearing Corporation of India)

For example at duration of 10 years, the rates as of March 31 were 7.14% and as on June 30 it’s 6.92%. The chart below is a plot of these rates:

What this means for you?

All things equal – as yields go up, the DBO goes down. This effect is diluted by adding in the other parameters that impact the obligation in different ways.

Most companies would have a duration of liability more than three years and therefore should see a rise in their DBO at the end of the first quarter of this FY. Companies with exceptionally high attrition rate (e.g. around 30-40% pa) could have a liability duration of lower than three years and they might see a small decrease in their DBO. However, for shorter duration schemes, the DBO is generally not that sensitive to discount rate fluctuations.

For companies which have set aside funds with an insurer, the changes in yield curve could also affect the value of those funds. Usually, a significant portion of these funds is invested in fixed income bonds issued by GoI or corporates, whose values also go down as yield curves rise, which could partially offset the benefit of decrease in DBO.

For more information about how discount rate is set for actuarial valuation, please read this post here.

Download our guide on transitioning to Ind AS from an employee benefits perspective by clicking on the picture below: